Mining is one of the few industries where the value of an asset is buried, quite literally, underground — and where the difference between a company worth billions and one worth nothing can come down to a few grams of metal per tonne of rock. For investors, operators, and companies looking at mining projects, the evaluation process is rigorous, standardized in important ways, and unforgiving of shortcuts. This article walks through what serious investors actually look for when they assess a mining asset, from the licenses and technical reports to the grades, geology, and market structures that determine whether a project is worth backing.

Site visit to an early-stage exploration project — the kind of ground-truthing that technical due diligence ultimately rests on

Licenses: The Legal Right to the Ground

Every evaluation starts with a simple question: does the company actually have the right to explore or mine this ground, and for how long? Two license types matter most.

An exploration license grants the right to search for minerals within a defined area for a set period. Investors examine its size, its remaining term, the renewal conditions, and whether the holder has met the minimum spending or work commitments required to keep it valid. An exploration license that is close to expiry, or that carries commitments the company cannot afford, is a red flag.

An exploitation license (also called a mining license or lease) grants the right to actually extract and sell minerals. This is the more valuable instrument, and investors scrutinize its duration, the royalty and tax terms attached to it, environmental conditions, and whether it can be transferred if the company is acquired. Because these licenses are granted by governments, political stability and the reliability of a country's mining code are part of the assessment. A world-class deposit in a jurisdiction where licenses are revoked arbitrarily is worth far less than a modest one in a stable country.

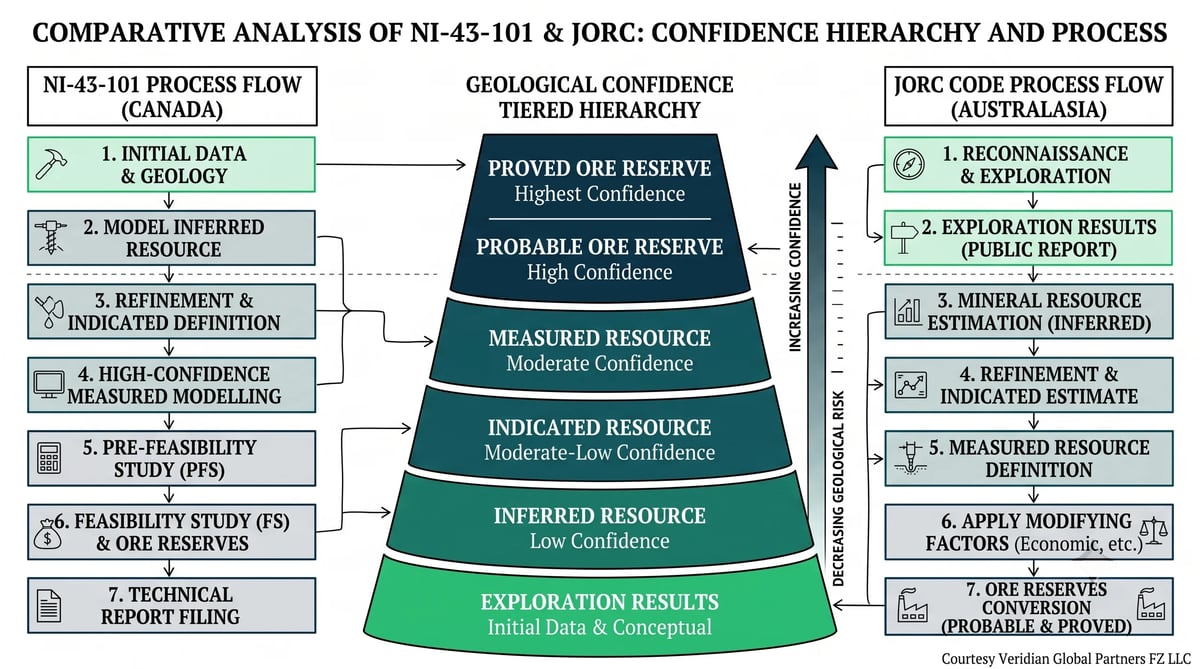

Technical Reports: NI 43-101 and JORC

Investors do not take a company's word about what is in the ground. They rely on standardized technical reports prepared by qualified professionals. Two reporting codes dominate globally.

NI 43-101 is the Canadian standard — formally, National Instrument 43-101, Standards of Disclosure for Mineral Projects. It governs how companies listed on Canadian exchanges disclose exploration results, resources, and reserves. It requires a formal Technical Report filed with regulators, prepared or supervised by a "Qualified Person" with defined credentials and experience.

The JORC Code is the Australasian equivalent — the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves, first established in 1971. It requires disclosures to be signed off by a "Competent Person." Both codes trace their definitions back to the same international framework (CRIRSCO), so the core vocabulary is shared.

One practical difference is worth knowing: NI 43-101 generally prohibits including low-confidence "inferred" resources in early economic studies, while JORC allows it with clear disclaimers. NI 43-101 is often described as a securities-disclosure code, while JORC is more focused on the resource itself. Both exist for the same reason — they were strengthened after historical fraud cases, most famously the Bre-X scandal of the 1990s, one of the largest core-sample fraud schemes in mining history.

Within these reports, investors look closely at how resources and reserves are classified. Resources are graded by geological confidence, in increasing order: inferred, indicated, and measured. Reserves — the portion of a resource proven to be economically mineable — are classified as probable and proven. A large "inferred resource" is interesting; a "proven reserve" is bankable. The migration of ounces or tonnes from inferred toward proven is, in many ways, the story of how a mining project matures.

Mineralized outcrop — the kind of surface geology that drives a geologist's initial hypothesis about what lies beneath

Feasibility Studies: PFS and DFS

As a project advances, companies commission increasingly detailed economic studies. Investors treat the study stage as a proxy for how de-risked a project is.

A Pre-Feasibility Study (PFS) is the first study rigorous enough to establish reserves. It tests mining methods, processing routes, and economics at a level detailed enough to demonstrate the project can work, though with wider margins of error.

A Definitive (or Detailed) Feasibility Study (DFS) is the highest level of study before a construction decision. It carries the tightest cost estimates, detailed engineering, confirmed metallurgy, and the financial modeling banks require before lending. A completed DFS with strong economics is what typically unlocks project financing.

Across both, investors focus on a handful of numbers: the projected all-in sustaining cost (AISC) of production, the net present value (NPV), the internal rate of return (IRR), the payback period, and the initial capital cost (capex). A high-grade deposit with poor metallurgy or crushing capital costs can still be a bad investment.

Active quarry operation — the practical reality behind the unit-cost and capex numbers in a feasibility study

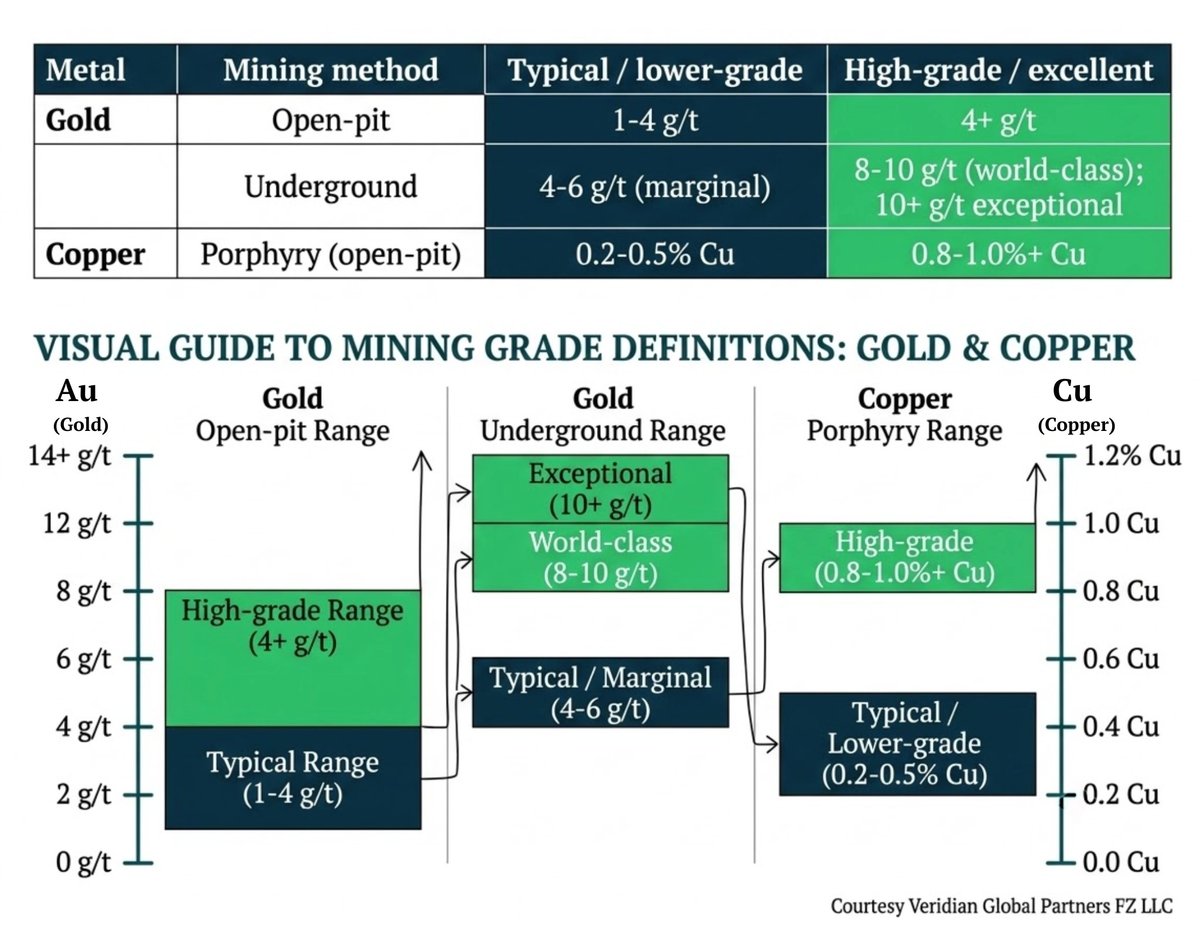

Grades: What "Good" Actually Looks Like

Grade — the concentration of valuable metal in the ore — is central to any evaluation, but it must always be read alongside depth and mining method. Open-pit mines are cheaper to operate, so they can be profitable at lower grades. Underground mines cost more, so they generally need higher grades to justify the expense.

The single most important number in a resource statement is often the cut-off grade: the minimum grade at which ore can be mined economically. Everything above it is "ore"; everything below is "waste." A shallow open-pit gold project might use a cut-off around 0.5 g/t, while a deep underground project might require 3.5 g/t or more to make the same economics work. When commodity prices rise, cut-off grades fall, and marginal material becomes ore — which is why grade can never be evaluated in isolation from price.

The table below gives broad, credible benchmarks for two of the most-scrutinized metals. These are general reference ranges, not hard rules — every deposit is different.

Gold benchmarks per the World Gold Council; copper porphyry benchmarks per USGS deposit data and industry sources.

For context: the world's large porphyry copper deposits — which supply well over half of global copper — often average around 0.5% copper or less, yet remain highly profitable because they are enormous and mined at massive scale. This illustrates a core principle: grade times tonnage times recoverability, set against cost, is what matters — not grade alone. For battery metals such as lithium and nickel, grade conventions differ (lithium is often reported as a percentage of lithium oxide, nickel as a percentage of contained metal), and benchmarks vary widely by deposit type, so investors lean heavily on project-specific studies rather than universal rules of thumb.

Underground mine infrastructure — the kind of capex-heavy build that separates a robust DFS from a paper project

Geology and Drilling: What Geologists Assess

Behind every grade number is geology, and this is where technical due diligence gets specialized. Geologists evaluate the deposit type (whether it is a porphyry, an orogenic vein system, a sedimentary deposit, and so on), because the type predicts size, shape, continuity, and how the metal is distributed. They assess the host rock, the structural setting, and the alteration patterns that often signal mineralization nearby.

The core tool for turning geological theory into hard data is drilling. Companies drill holes across a deposit and assay the recovered core to measure grade at depth. Investors pay attention to the spacing of drill holes (tighter spacing means higher confidence), the consistency of results between holes, the width of the mineralized intersections, and whether the deposit remains "open" — meaning mineralization continues beyond the drilled area, hinting at growth potential. Metallurgical testing matters just as much: ore that is chemically difficult to process ("refractory") can turn a high grade into a low profit.

A drill rig in the field — the data-collection work that turns an exploration target into a resource statement

Who the Major Players Are

The mining world runs on a spectrum from tiny explorers to global giants. At the top sit the major producers — diversified companies like BHP and Rio Tinto, and large specialists like Freeport-McMoRan in copper or Barrick in gold. These companies operate flagship assets such as BHP's Escondida in Chile (the world's largest copper mine) and increasingly acquire promising projects rather than discovering everything themselves. Alongside operators, a distinct class of royalty and streaming companies finances mines in exchange for a share of future production, offering investors commodity exposure without operational risk.

Site operations — the day-to-day reality of bringing a project from feasibility into production

Mining Capital Markets and the Junior Model

Most of the world's mineral discovery is done not by the majors but by junior mining companies — small, exploration-focused firms that typically have market capitalizations under $500 million and, crucially, often generate no revenue. Their business model is high-risk: raise money, drill, and hope to find a deposit valuable enough to either develop or sell to a major. Industry estimates suggest only about one in a thousand exploration projects becomes a viable mine, which is why juniors live and die by their news flow and their ability to keep raising capital.

Juniors cluster on two exchanges above all: Canada's TSX Venture Exchange (TSXV) and the Australian Securities Exchange (ASX). The reasons are practical. These exchanges have listing requirements tailored to early-stage, pre-revenue explorers that would never qualify for a senior board. They host deep pools of specialist investors and analysts who understand geological risk. According to TSX data, roughly 40% of the world's public mining companies are listed on the TSX and TSXV, and Canada accounts for a large share of global mining financings. Canada also offers tax-advantaged "flow-through shares" that channel investment into exploration. Australia's ASX brings similar depth, particularly for battery-metals and gold explorers operating across the Asia-Pacific. Juniors typically raise money through private placements to accredited investors, and successful ones can eventually "graduate" from the TSXV to the senior TSX as they grow.

Where Mining Finance Is Heading

Two forces are reshaping how mining is financed and evaluated. The first is the energy transition. Demand for copper, lithium, nickel, and rare earths — the metals behind electrification and grid infrastructure — is driving premium valuations for projects in these commodities, especially those located in stable, allied jurisdictions. National-security concerns around critical-mineral supply chains are pulling government and strategic capital into a sector that was, until recently, financed almost entirely by private markets.

The second is the growing role of alternative financing and partnerships. Rather than relying solely on repeated, dilutive equity raises, juniors increasingly secure offtake agreements, streaming and royalty deals, and cornerstone investments from major miners and commodity traders. These arrangements advance projects faster and send a strong signal: that a sophisticated industry participant, with its own technical team, has examined the asset and chosen to back it.

Through all of this, the fundamental due-diligence parameters remain remarkably constant. Investors weigh the quality of the license and the jurisdiction, the credibility of the technical reports, the grade set against depth and cost, the geology and drilling confidence, the metallurgy, the project economics in the PFS or DFS, and — repeatedly cited by experienced resource investors as the single most important factor — the quality and track record of the management team. As the veteran investor Rick Rule has put it, success in junior exploration is more a function of people than of property.

Mining rewards those who read the technical detail carefully and treat grade, geology, and economics as one connected picture rather than a single headline number.

Recommended Resources

- NI 43-101 (Canadian Securities Administrators): www.securities-administrators.ca

- JORC Code (official site): www.jorc.org

- CIM Definition Standards (resource/reserve definitions): www.cim.org

- TSX Venture Exchange: www.tsx.com

- Australian Securities Exchange (ASX): www.asx.com.au

- Trading Economics (live commodity prices): tradingeconomics.com/commodities

- World Gold Council: www.gold.org

- U.S. Geological Survey (mineral deposit data): www.usgs.gov

Disclaimer: Nothing in this article constitutes investment advice, and the author is not a qualified geologist. The content is provided for general commentary and informational purposes only. Grade benchmarks and figures are general reference ranges drawn from public industry sources and will vary by deposit, jurisdiction, and market conditions. Anyone evaluating a mining investment should rely on qualified professional and technical advice and the project's own compliant technical reports.

Get In Touch

Contact Us

Article Written By

Martin Kocher

Managing Partner, Veridian Global Partners